Got a 401(k)? Congrats, you’re an investor!

Retirement saving is really just another form of investing. Time to treat it that way.

Dan Muse

March 14th, 2023

Blog | Got a 401(k)? Congrats, you’re an investor!

tl;dr

Retirement saving is just another form of investing

If you have a 401(k) through work, you might not think of it that way

Strategize with your retirement savings just as much as other investments

Got a 401(k)? Congrats, you’re an investor!

We put a pretty narrow box around the term “investor.”

Specifically:

You’ve got a portfolio with a brokerage

… with a handful of investments

… that you chose yourself

… and actively manage it on a regular basis

If you’re reading this, that’s probably you (or just about). You’re our kind of people, honestly. We built Finiac with you in mind.

But when it comes to regular people with money in the markets, that describes only a handful of folks. There’s a whole swath of people out there that make up a huge chunk of the markets and generally don’t even consider themselves “investors.”

We’re talking people with retirement accounts.

401(k), 403(b), Roth IRA, SEP IRA. Every one of these is just a vehicle to put money out there that you hope to grow—just like your brokerage account.

So we started wondering: why don’t these folks think of themselves as investors?

A few possibilities:

Retirement money doesn’t feel like yours

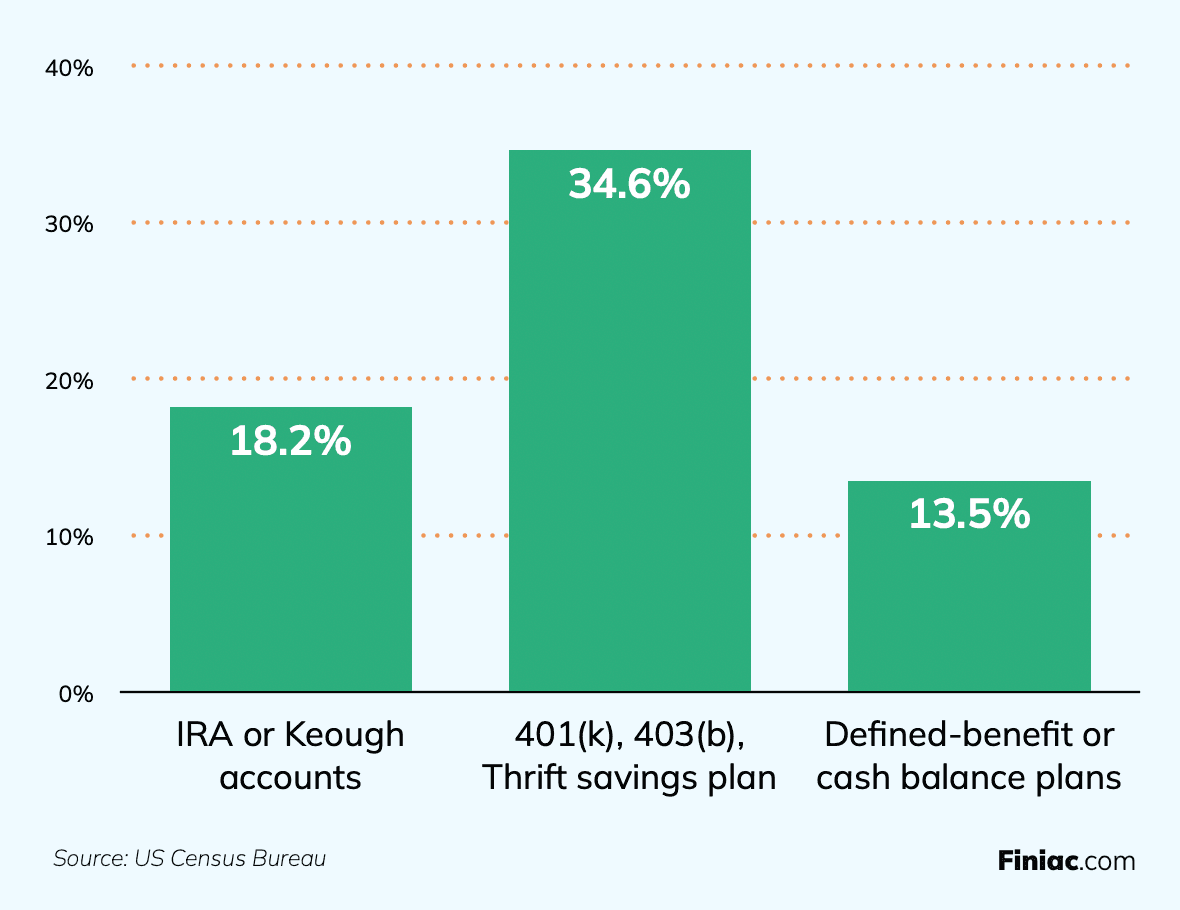

The most popular type of retirement account in the US is a 401(k)—about 35%, vs. 18% for IRAs or Keough accounts (according to the US Census Bureau.

And most people with 401(k)s got them through an employer, which full administrates the account on their behalf.

Most employees simply have money rerouted from their paychecks directly into the 401(k) account, so it never actually hits their pocket.

The effect being that it doesn’t even feel like your money.

When it comes to investing, that’s a major problem.

You can’t access it for decades

This is basic liquidity—if you’ve got money in a brokerage account, it might not be in your pocket, but you could sell and turn it into cash on hand pretty quickly.

Not so with retirement accounts. Almost all of them carry penalties for withdrawing before a certain date, which, for most of your working life, is many years off.

It contributes to that effect we just talked about: that money might belong to your future self, but it certainly doesn’t feel like yours.

You don’t know what you’re invested in

We’ve got some really on-top-of-their-game people using Finiac, so if you’re reading this, you might very well know exactly the composition of your retirement account.

But the average owner of a 401(k) has a tough time even finding out what they’re invested in.

On Day 1 of your new job, you often get a menu of funds to choose from, with a bit of information about performance or the balance of sectors on offer. You choose the one that looks good, and then let it ride.

Who’s managing that account? Rebalancing when needed? Monitoring performance on the regular?

It depends—could be someone at your company, could be a third-party account sponsor, could be the institution (Vanguard, Blackrock, etc.) that created the fund.

Point being, if you’re an employee, and don’t have experience otherwise investing, then you might have little or no knowledge or control over where your money (and again, it’s your money!) is going.

Excellent question. A few others

“But retirement investing isn’t like my everyday portfolio.”

We totally get that. You’re right have different expectations of a retirement account than your fun-money Robinhood account. For one thing, you shouldn’t need to babysit it nearly as much. One of the attractive things about retirement saving is that you don’t need to worry about it day to day.

A couple of points to follow up on this, though:

You should know how your money is influencing the market.

We hear it all the time, but it’s true: money talks. You should know what yours is saying. Invest in what you believe in. It’s true for your brokerage account, just like it is for your retirement account.

You deserve to know how your account is doing.

If you want to check on your brokerage account, often enough you just open an app. Two seconds, and you know exactly who you’re doing. It’s often a lot tougher with retirement accounts. But depending on where you’re at in your career, you might have more money in the retirement account, and yet have way less insight as to how it’s doing.

That’s an imbalance that needs correcting. You deserve to know.

Takeaway: retirement saving is investing

The care that we put into building portfolios—analysis, due diligence, strategic thinking—should go retirement, too.

Right now, we’re developing tools that’ll make it even easier for retirement account holders to evaluate those investments.

Get curious. If you know what’s in your retirement portfolio, draft it up in Finiac and take a look at the metrics. You might be surprised at what you find.

3 actions to improve your retirement planning today

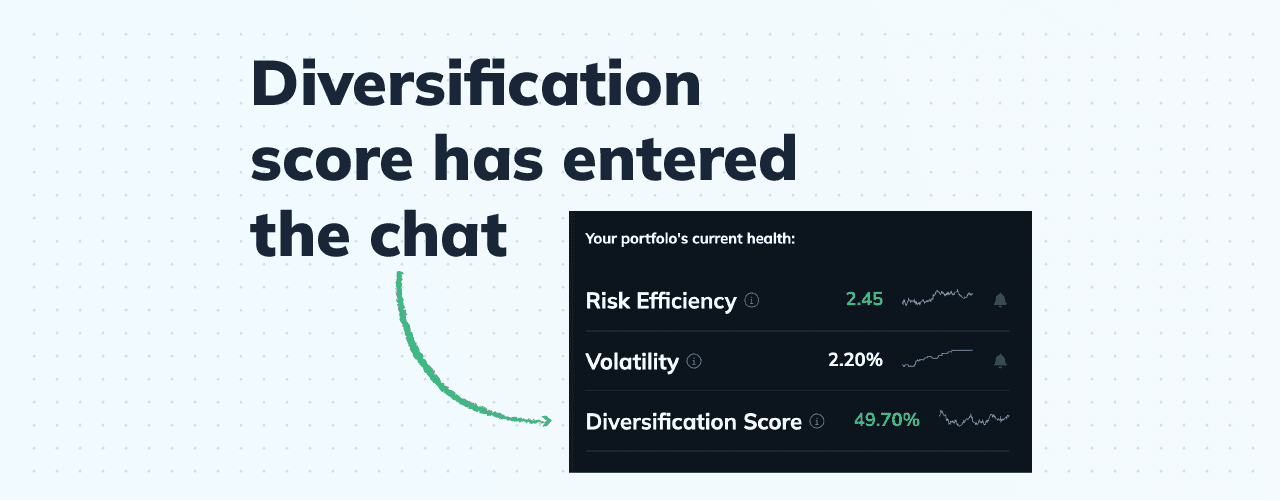

Make sure you’re diversified! Especially in 401k plans, it's easy to have multiple assets that overlap by a large amount. Keep things diversified to keep your risk as low as possible. Use Finiac’s Diversification score to see how you’re doing on this front.

Check up on your fees. Many retirement accounts offer mutual funds as a way to buy into pre-made baskets of stocks. These come with fees, which can eat into your long term gains. Make sure you know how much you're paying, and evaluate lower-cost options if yours feel too high.

Rebalance regularly. The markets and world economy are changing all the time, and that means your portfolio is also changing with it. Rebalance at least yearly (quarterly if you're investing for under 10 years) to make sure your allocations stay optimized for the current state of things.

Don't fall prey to loss aversion

Design better portfolios with RiskSmith

Related Posts